When Great Businesses Go on Sale

When Great Businesses Go on Sale

Every market cycle develops its own irresistible story. Today that story is artificial intelligence.

There is little doubt that AI will change industries and create enormous value over the coming decade. But markets have a habit of taking good stories and pricing them as though nothing can possibly go wrong.

That is where investors should become cautious.

The recent performance of global equity markets has become extraordinarily narrow. A small group of technology companies has driven a disproportionate share of returns, leaving many disciplined quality investment strategies looking disappointing by comparison.

That has created a dangerous illusion. It appears as though quality investing has stopped working.

We would caution that the evidence suggests otherwise.

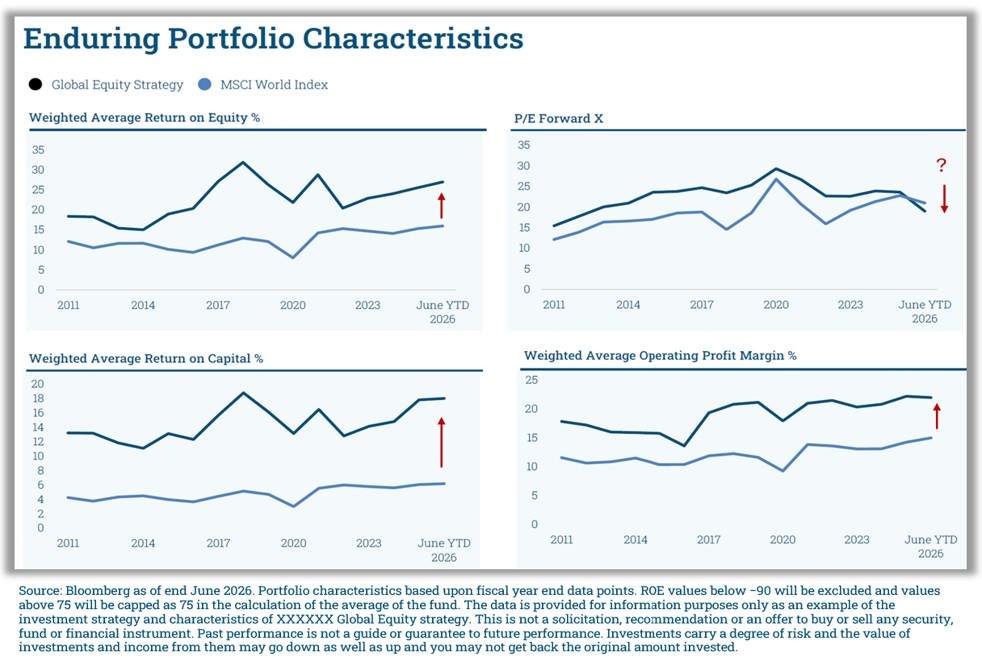

One global quality portfolio that we have been following closely continues to own businesses with higher returns on equity, higher returns on invested capital and stronger operating profit margins than the MSCI World Index. In fact, these positive factors have widened rather than narrowed over recent years.

The businesses have become more attractive investments, but their valuations have become cheaper.

Yet despite owning better businesses according to almost every metric, the portfolio now trades on a lower price-to-earnings ratio than the index. Think about what that means.

The market is currently asking investors to pay more for businesses with weaker fundamentals because they are associated with a compelling future narrative, while simultaneously asking investors to pay less for businesses already generating realised profits today.

That is unusual. History suggests these periods rarely last forever.

Markets eventually reconnect price with business fundamentals. When expectations become too optimistic, even small disappointments can lead to sharp repricing. Companies priced for perfection have very little margin for error.

Companies generating consistent profits, however, do not require a perfect future. They simply need to continue doing what they have already demonstrated they can do.

This is why investing is often uncomfortable. The greatest temptation comes precisely when your long-term discipline appears to be failing while everyone else seems to be making easy money.

That is when investors abandon carefully constructed strategies and chase yesterday’s winners. Fear of missing out replaces patience. Recent performance replaces valuation. Stories replace evidence.

These are often the moments when future returns are quietly improving for the patient investor. Sometimes the most valuable thing you can do is simply zoom out.

Markets have always swung between excessive pessimism and excessive optimism. Today’s concentration may eventually prove justified, or it may not. Nobody knows with any certainty.

What we do know is that paying increasingly higher prices for increasingly optimistic assumptions has rarely been a reliable long-term investment strategy. The reward for disciplined investing has never come from following the crowd.

It has come from having the patience to endure periods when the crowd appears to be right.

Eventually, markets tend to remember what really creates value. Businesses do. Not stories.

Markets periodically confuse exciting stories with durable value.

Disciplined investors are rewarded not by chasing what has already happened, but by remaining patient when prices temporarily disconnect from business fundamentals.

Written by Marius Kilian