Smart Investors Avoid the Thrill of the Chase

We like to think of ourselves as rational decisionmakers making decisions that will serve in our own best interest. Your future will be the result of your actions not your intentions. Why do we persist with behaviours that dilutes our future opportunities?

The body of evidence is clear that investors frequently move assets to funds that has experienced stronger recent performance. This is evident from the flow of funds in all markets. Researchers agree that fund flows are strongly correlated with past performance.

Itzhak Ben-David, Jiacui Li, Andrea Rossi, and Yang Song looked at the behaviour of individual investors in their study “What Do Mutual Fund Investors Really Care About?”, published in the July 2021 issue of The Review of Financial Studies.

To determine if individuals are just naïve performance chasers, unaware of the financial literature, or whether they are sophisticated investors Ben-David, Li, Rossi, and Song examined mutual fund flows spanning the period 1991-2017. Following is a summary of their findings:

- Individuals are simple decision makers who invest using easily obtainable information and do not adjust fund performance using asset pricing models.

- Simple performance-chasing behaviour explained the major flow patterns observed in the mutual fund market.

- Individual investors do not engage in sophisticated learning about managers’ alpha-generating ability and do not distinguish between fund returns attributable to risk factor exposure versus alpha.

- Morningstar star ratings and past unadjusted returns best explained which funds attracted flows, with both ratings and unadjusted returns having strong independent effects on flows—fund rankings based on alphas from common asset pricing models do not help to predict flows better than unadjusted returns-based rankings. In some econometric specifications, funds with high alphas received significantly lower flows than funds with high unadjusted returns.

- Furthermore, they present evidence consistent with investors following Morningstar blindly, regardless of the way the ratings are constructed.

Investors would rather invest in winning funds than losing funds. In the fund selection process, it intuitively feels easier to turn to “highly rated” funds with the expectation that such a process will ultimately lead to success. But does past performance provide any tangible information to investors going forward? This has been the topic of many research papers.

Investors would rather invest in winning funds than losing funds. In the fund selection process, it intuitively feels easier to turn to “highly rated” funds with the expectation that such a process will ultimately lead to success. But does past performance provide any tangible information to investors going forward? This has been the topic of many research papers.

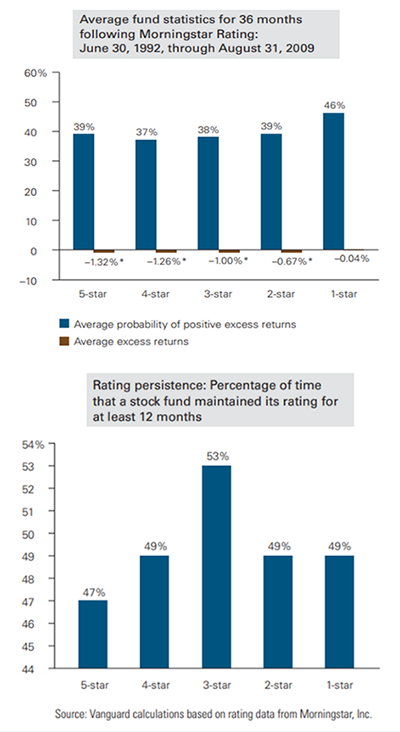

Vanguard published their findings in a June 2010 report. They looked at the excess returns over a 3-year period following a given rating. How did funds perform in the subsequent 3-year relative to a benchmark after they received a star rating: from 1 star to 5 stars? No surprises here.

On average, 39% of funds with 5-star ratings outperformed their style benchmarks for the 36 months following the rating, while 46% of funds with 1-star ratings outperformed their style benchmarks for that period. More than 60% of 5 star rated funds underperformed the benchmark in the following 3 years.

The top-rated funds are shown to have generated the lowest excess returns across time, while the lowest rated funds generated the highest excess returns. Investors, on average, do not benefit from basing their decisions solely on historical quantitative performance metrics.

Persistence Scorecard

Then there is the matter of persistence in performance. Nobody stays at the top.

The graph shows the likelihood that a stock fund with a given rating will still have that rating at the end of the next 12 months. Vanguard found that most funds had less than a 50% chance of earning the same rating just 12 months following the initial rating. 5-star funds showed the lowest probability of maintaining their rating.

Being Human

It’s hard to ignore funds that have crushed the competition in recent years. This behaviour feels intuitive as every investor’s goal is to maximise return. Performance chasing is bad for your financial welfare. The average investor underperforms the funds that they were invested in.

Performance chasing can only succeed if past performance can predict future performance. We are compelled by regulation to disclose this not to be true. Various studies confirm that it is folly to believe that taking action based on past performance is a worthwhile activity.

Behaviourally we tend to confuse activity with achievement. It feels right to do something when we experience stress. This is normal as your “rational brain” (Pre-frontal Cortex) takes the backseat when you experience stress. Another part of your brain (Amygdala) kicks in right on cue when you experience stress and triggers the so-called “fight or flight” response. This is not just an emotional experience it is also a physiological reality. Your body is immediately flooded with a cocktail of hormones that includes adrenaline and cortisol which primes your body for action.

Doing nothing when you experience stress goes against your nature. Doing nothing when you have a long-term plan and strategy is the right thing to do. How do we moderate this behaviour as it does not serve our own best interests?

Managing expectations

It is better to structure and maintain portfolios that accept and anticipate market dislocations that meet both the behavioural and economic needs of investors. It is important that advisors discuss with investors plans of action for market disruptions in advance to ensure investor commitment when market challenges inevitably emerge. It is better and less trouble to have these truthful conversations with clients than waiting for the next market downturn to force the issue. Once a volatility event occurs, it may be too late to course correct and educate. When fear take hold people respond differently. We present ourselves differently in different situations. Set up a structure in advance that you can fall back on.

Talking someone of a cliff with education is not going to work in most cases. You need a mindful process and narrative that helps clients to appreciate the history and nature of markets. This understanding could help mitigate behaviour when fear abound. Everybody has a breaking point. The advisor’s job is to extend that breaking point. This would serve as a vaccine prior to when unexpected volatility sets in.

We are evolutionary hardwired to be emotional investors. It is the reality of being human. Manager performance is usually not a “manager” problem. It is usually a portfolio construction and investor behaviour problem. It is better to have a well-considered strategy and structure that is defined by the investors long-term goal and then sticking with it. Unfortunately, it feels less exciting than chasing the markets and “best performing funds”.

Successful investing and successful client relationships often rely more on taming emotions than on taming the markets.

The above article was written by Marius Kilian.