“Investing Like Buffett” Is Easier Said Than Done

Warren Buffett may be the most quoted investor of all time.

He is also perhaps one of the least understood.

Everyone admires the outcome. Everyone wants Berkshire Hathaway-like returns. Investors enthusiastically repeat Buffett’s sayings, celebrate long-term compounding, and profess a commitment to patience and discipline.

But few truly appreciate what that journey actually requires, because Buffett’s success was never simply about buying good businesses.

It was also about enduring long periods of discomfort without abandoning the process.

That is the part most people conveniently overlook.

Investors love to quote Buffett when markets are rewarding their philosophy. They love to speak about “being greedy when others are fearful,” “thinking long-term,” and “staying the course.”

Investing like Buffett is easy only in theory. In practice, Buffett’s journey has repeatedly included long stretches where his approach appeared out of touch, old-fashioned, or simply wrong.

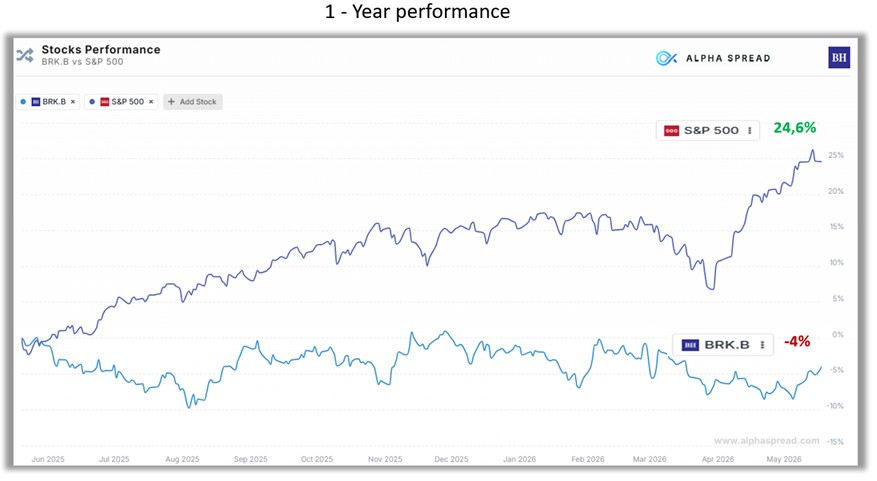

Even Berkshire Hathaway has experienced extended periods of relative underperformance.

Over the past calendar year, Berkshire Hathaway (BRK.B) significantly trailed the S&P 500, underperforming by more than 28%.

To investors focused only on recent returns, that can appear alarming. It creates the familiar temptation to ask whether Buffett had “lost it,” whether the strategy still works, or whether something fundamentally changed.

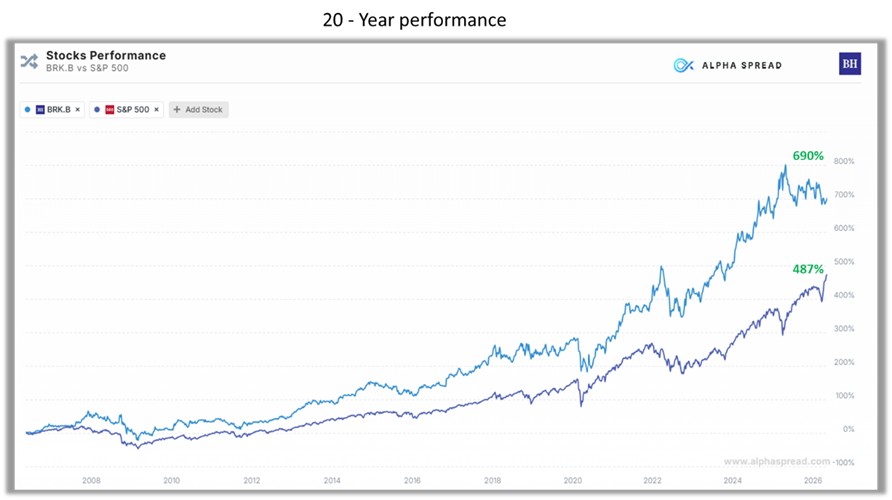

Yet zoom out and the picture changes dramatically.

Over the past twenty years, Berkshire Hathaway delivered cumulative returns of approximately 690%, compared with roughly 487% for the S&P 500.

The difference is substantial, but what is often forgotten is that those excess returns did not arrive in a smooth, uninterrupted line. They came with periods of frustration, doubt, and relative disappointment. That is not an exception.

That is the reality of the journey. The lesson is not really about Berkshire Hathaway.

The lesson is that long-term outperformance almost always requires enduring periods of short-term underperformance. You do not receive the rewards of a strategy without also accepting the conditions attached to it.

Investors often say they want long-term returns. What they frequently mean is that they want long-term returns without temporary discomfort. But markets do not work that way.

Every successful investment philosophy carries a behavioural cost. Every approach will eventually test your patience, challenge your conviction, and make you question whether you should abandon it.

That is precisely where discipline matters.

Markets move through cycles. Narratives change. Today’s certainty often becomes tomorrow’s forgotten story.

Your philosophy is what remains. Choose a strategy. Understand why it works. Accept the periods where it may not.

Then commit to it through time.

Written by Marius Kilian

Source

* www.alphaspread.com/comparison, 19 May 2026