Markets, Instincts and Bad Decisions

A big market decline is an unnerving and painful experience.

It triggers emotions that pulls our attention and perspective into a very narrow space. In times like these it always feels like the world is coming to an end. But it never does. Declines have always been temporary. This time will not be different. This is not the first time the markets have declined sharply and it sure won’t be the last.

When markets decline it is difficult not to default to survivalist thinking.

The deepest human evolutionary instinct is survival. From a behavioural perspective we are not wired to make good financial decisions under stress. Investment decisions should be guided by insight and not by instinct. The space between experiencing a stimulus and responding to it is called choice. If these choices are being made mindfully it will give you the time to make them skilfully. Skilful decisions lead to the better outcomes you desire.

Our understanding of the market does not change its cycles, it merely gives us the capacity to have an informed perspective that drawdowns are a normal and inevitable part of the journey to harvesting the higher returns that it has historically provided in the longer term. Markets and the future are by its very nature uncertain. But humans crave certainty…. even a false sense of certainty seems to be more comforting than uncertainty.

Nobody can make predictions about markets or the future with any consistency. Nobody. We know this to be true. But still, we have a deep desire to listen to market commentators that have no interest in our future personal financial outcomes. The bad news gets all the attention, and our better perspective suffers as a result. We should not tune into the noise. We suffer unnecessarily when we do.

“These mountains that you are carrying, you were only supposed to climb.” – Najwa Zebian

“Buy low, sell high” sounds great in principle, but based on the history of asset class flows investors consistently do the opposite. We tend to time our beatings perfectly. We seem to oscillate between FOMO (fear of missing out) and fear. When markets run, we experience FOMO. Fear of missing out replaces fear of losing money. When markets decline, we experience fear. This feeds into value destroying behaviours.

We intentionally start of by committing to a long-term plan and a target portfolio only to evaluate it against:

- “Beating the market” in good times and

- “Beating cash” in the bad times.

When markets decline clients predictably question their long-term portfolios relative to cash. Based on human behaviour this is both predictable and understandable. From a financial planning perspective, it is dead wrong and unproductive.

What is the financial plan trying to solve?

If it is for a long-term commitment, then your priority is to focus on the long-term risk which is inflation. Don’t get side-tracked by the short-term risk that is the price volatility of the markets. It will have an emotional impact on you and that is OK. Acting on it is not.

The real problem to solve in the long-term is: “How much will the money in my hands be worth in purchasing power after tax and inflation when I need to fund a future commitment?”

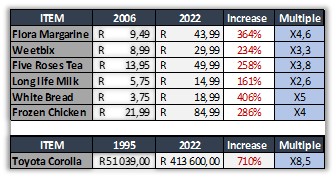

In the graph below we considered the impact of inflation over the long-term.

As mentioned in a previous article – the future is a real place, and you will live in it. Inflation does not care for your comfort with short-term volatility. We all would love to have a “sleep well portfolio”. In the real world this usually translates into you not having a “eat well portfolio” in the longer term. Wanting more of one thing usually means settling for less of another. All your decisions involve a trade-off. It has consequences. At least do it mindfully.

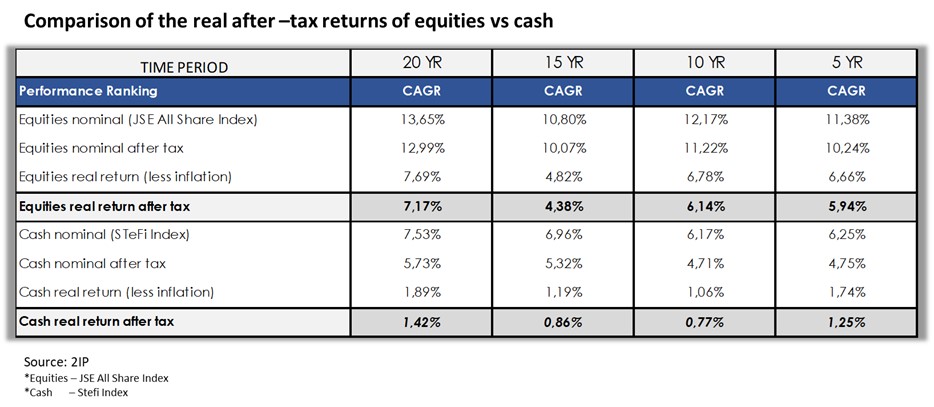

Let’s consider the logic of the “comfort of cash”. The graph below compares equities vs cash over various time periods.

From a tax perspective we applied the rates prescribed in terms of the “5 fund approach” set out in the Long-Term Insurance Act:

- 12% flat rate Capital Gains Tax on the equity at the end of each relative period.

- 30% flat rate Income Tax on the interest on an annual basis.

The clear observation is that cash underperforms the markets over each period. It underperforms equity by factors in real terms after-tax. For all the time periods considered above the equity market experienced large draw downs. It still provided the best after-tax real return.

The comparison above is not to advocate at the extreme, but rather to provide context from a long-term planning perspective that typically benefits from a diversified portfolio structured with a target return in mind.

Your money is earmarked for a specific personal future goal. Beating the best performing asset class consistently cannot be a goal. A well-structured portfolio is based on the acknowledgment that both the markets and the future are uncertain. Nobody can divine the future nor need to. Based on the evidence of the past you structure a portfolio that presupposes that there will be cycles (good and bad). You select an asset allocation that should give you the highest probability of meeting your future objective. Anything else is based on ignorance or arrogance. Neither of these two traits are profitable in the long run.

When the water is turbulent it’s difficult to see clearly. When you don’t see the bottom, everything feels like an abyss no matter how shallow it is. Investment advice cannot be based on predicting or timing the future. It can only be based on the evidence of history and experience.

Your long-term outcomes are determined more by how you manage yourself as opposed to how you manage the markets. The truth is that you cannot manage the markets. You can only harvest the returns that it gives over time. Worrying about it through the cycle’s changes nothing.

Don’t let your nerves get the better of you.

“If it’s out of your hands, it deserves freedom from your mind too.” – Ivan Nuru

The advisor’s job is to advise their clients through both good and bad times. This requires investment literacy and a grounding in evidenced based investing. History is a good guide.

“Having both an intellectual and emotional understanding of bear markets can help us offer life-altering advice during challenging times”. – Morgan Ranstrom

Any investment plan that relies on the ability to call the tops and bottoms of the market is downright dangerous.

End of June the JSE ALSI was down -8,2% year to date. End of July it was only down -4,4% year to date.

What will happen next?

The truth is I don’t know. Nobody knows. Don’t try to outsmart the markets in the short term. It is better to out-behave everyone else who think they have an informational advantage.

Follow an approach that stacks the odds for success in your favour and then stick to it. Better behaviour and a long-term bias would serve your interest best.

References:

- www.thesouthafrican.com/lifestyle/then-and-now-food-prices-in-south-africa-compared-to-10-years-ago

- www.iol.co.za/motoring/industry-news/heres-how-much-south-africans-paid-for-new-cars-25-years-ago-1995

DISCLAIMER

The opinions expressed in this article are for general informational purposes only and are not intended as specific or personalised financial advice.

The author shares ideas and information curated from various sources that is intended to contribute to greater awareness and perspective regarding conversations about investments and investor behaviour. The article reflects the personal opinions, thoughts and research of Marius Kilian. It is regarded as a continuous learning process. Past performance is no guarantee of future results.