How the “Flaw of Averages” Distorts Investor Decision-Making When Planning for Future Goals

Consider the case of the statistician who drowns while wading through a river that he calculated to be, on average, three feet deep. If he were alive to tell the tale, he would warn that plans based on assumptions about average conditions usually go wrong. This story illustrates a crucial concept: focusing solely on averages can lead to dangerous oversights.

Most planning—whether for personal finances or IT projects—relies heavily on average expectations. Budgets, timelines, and projections are often built around these averages, yet they reflect just one point within a range of potential outcomes. However, variability is a constant, and outcomes often diverge from the average.

Most planning—whether for personal finances or IT projects—relies heavily on average expectations. Budgets, timelines, and projections are often built around these averages, yet they reflect just one point within a range of potential outcomes. However, variability is a constant, and outcomes often diverge from the average.

Sam Savage, a professor at Stanford University and author of The Flaw of Averages: Why We Underestimate Risk in the Face of Uncertainty, explores how decision-making becomes flawed when we rely too heavily on average numbers. “Plans based on average assumptions are wrong on average,” Savage explains. Relying on a single average figure creates a false sense of certainty in an uncertain world.

The Trap of Averages in Planning

The Flaw of Averages occurs when a single number—representing an uncertain future quantity—is used in planning, ignoring the variability that defines real outcomes. Take an IT project, for example. When an executive asks, “How long will it take the programmers to finish the code?” the developers may offer a timeline of 3 to 9 months. Often, the average of 6 months becomes the official project estimate.

However, real-world projects rarely proceed as expected. If one of the five programmers falls behind, the entire schedule and budget can collapse. This is because the various tasks in a project are interconnected, and delays in one area affects the entire process.

In its simplest form, an average is a single number that represents a distribution of numbers. It does not capture the full storey.

Why Averages Distort Investor Expectations

Uncertainty plays an even more critical role in personal financial planning and investing. Investors often anchor their expectations to historical averages. For example, the U.S. stock market has delivered a long-term average return of between 8-10%. At first glance, this seems like a solid benchmark for planning.

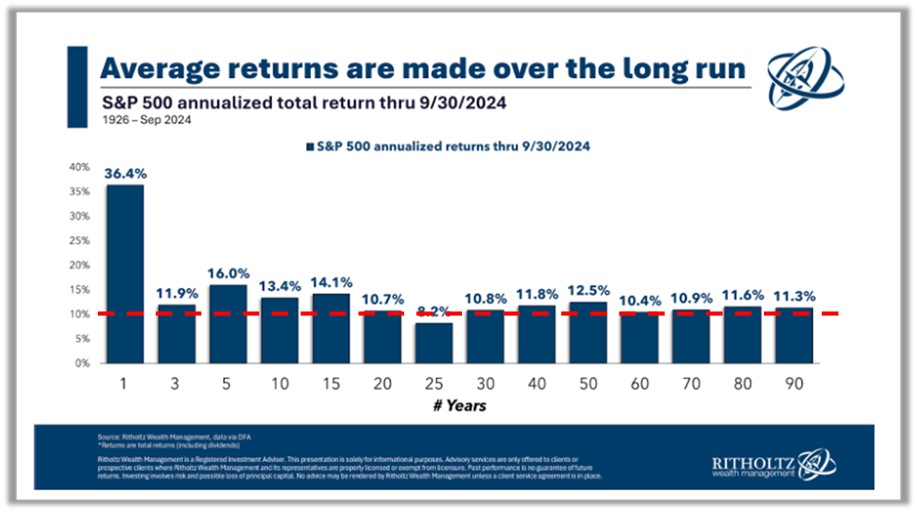

If you consider the graph below, provided by Ben Carlson, then you will find comfort that in the long-term “average number”. Even the 3-year number is close to the average which is surprising if you consider that 2022 was a negative 18%.

The context that is often lost is how we get to the long-term average. To harvest the long-term average, you need to be invested for the full period.

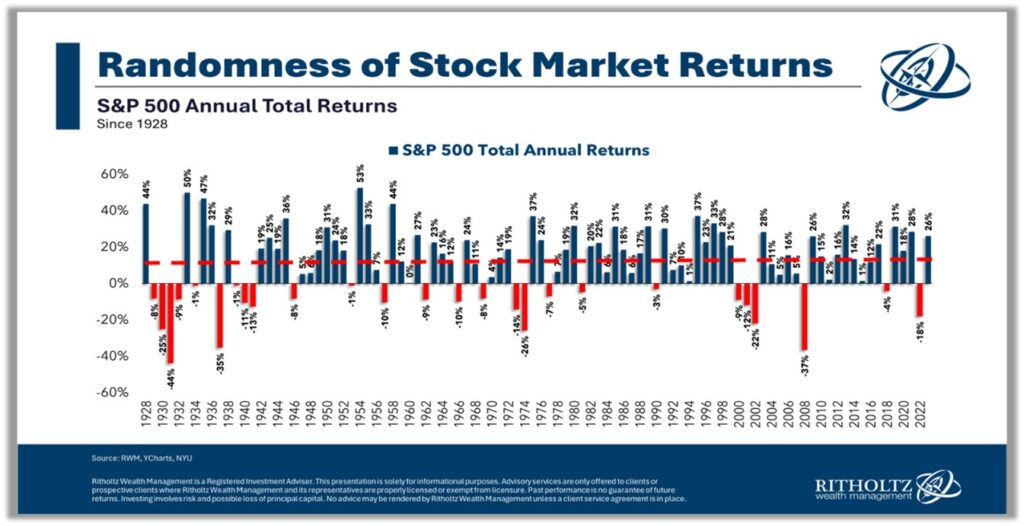

The graph below shows the actual experience of how we got to “the average”. A crucial lesson here is that achieving long-term returns requires staying invested throughout market cycles. Markets overshoot and undershoot the average regularly, making it unrealistic to expect the “average” outcome in any given year. In fact, since 1928, the 8-10% range has only been observed four times.

Dallas, Texas, is often described as having a pleasant annual average temperature. However, living through its four distinct seasons reveals a different reality: summers are intensely hot, and winters can be quite cold. The “pleasant average” rarely reflects the actual day-to-day experience.

Adaptive Planning: Embracing Variability

The sequence of returns—the order in which gains and losses occur—can profoundly affect financial outcomes. This is particularly important in retirement planning, where early negative returns can derail an entire strategy. Since investors have no control over market sequences, they must build adaptive strategies that accommodate uncertainty.

The flaw of averages reminds us that averages are not guarantees. While long-term averages provide useful benchmarks, they should not form the sole basis of decision-making. Instead, investors need a flexible approach that accounts for market variability and unforeseen life events. In an unpredictable world, a rigid plan is more likely to fail.

Behavioural Challenges and Investment Success

Investor behaviour plays a critical role in long-term success. Too often, people measure their portfolio’s performance against short-term market movements, leading them to act impulsively and against their best interests. Behavioural research shows that the “average investor” tends to underperform due to poorly timed decisions—selling during downturns and missing out on subsequent recoveries.

–As Morgan Housel notes, “All past declines look like an opportunity; all future declines look like a risk.”

Beating the behaviour of the “average investor” is key to achieving superior returns. Success in investing is less about predicting market movements and more about setting realistic expectations and managing emotions effectively.

This concept is known as behavioural alpha—the consistent, reliable excess return generated through disciplined and thoughtful investor behaviour. Unfortunately, negative behavioural alpha—the loss of returns due to impulsive decisions—tends to be persistent.

Investors who avoid knee-jerk reactions and maintain a long-term perspective are far more likely to stay on track and achieve their financial goals.

The above article was written and adapted by Marius Kilian.

Sources

*” The Flaw of Averages: Why We Underestimate Risk in the Face of Uncertainty”, Sam L Savage, John Wiley & Sons.

*”Long-Term Stock Market Averages, Ben Carlson, awealthofcommonsense.com, 13 Oct 2024